網上版請按此

Tapping global payment market by integrating regulatory systems

According to the Economist, in the past 10 years from 2011 to 2021, Singapore was ranked the seventh among the 12 largest cities with the most unicorns (startup companies valued at or over US$1 billion) in the world, the third-highest ranking among Asian cities.

You may be familiar with the various essentials for creating a unicorn, including nearby talent pools (Bengaluru of India, ranked the fourth city in the world with the most unicorns, has nearly 70 engineering colleges), an open attitude to new ideas and foreign talents (nearly 60% of the most valuable tech companies in the United States were founded by immigrants or their children), active venture capital funds, government support (funding and contracts), and more.

I believe it is also important to have policies that keep pace with time for retaining talents and attracting funds. Paul Li, President of Hong Kong Fintech Industry Association and a cross-border payment expert shared some of his observations that Singapore has attracted many unicorns to set up Asia-Pacific headquarters there in recent years, as its financial technology (FinTech) policies are more in line with the digital economy, resulting in FinTech talents naturally heading there.

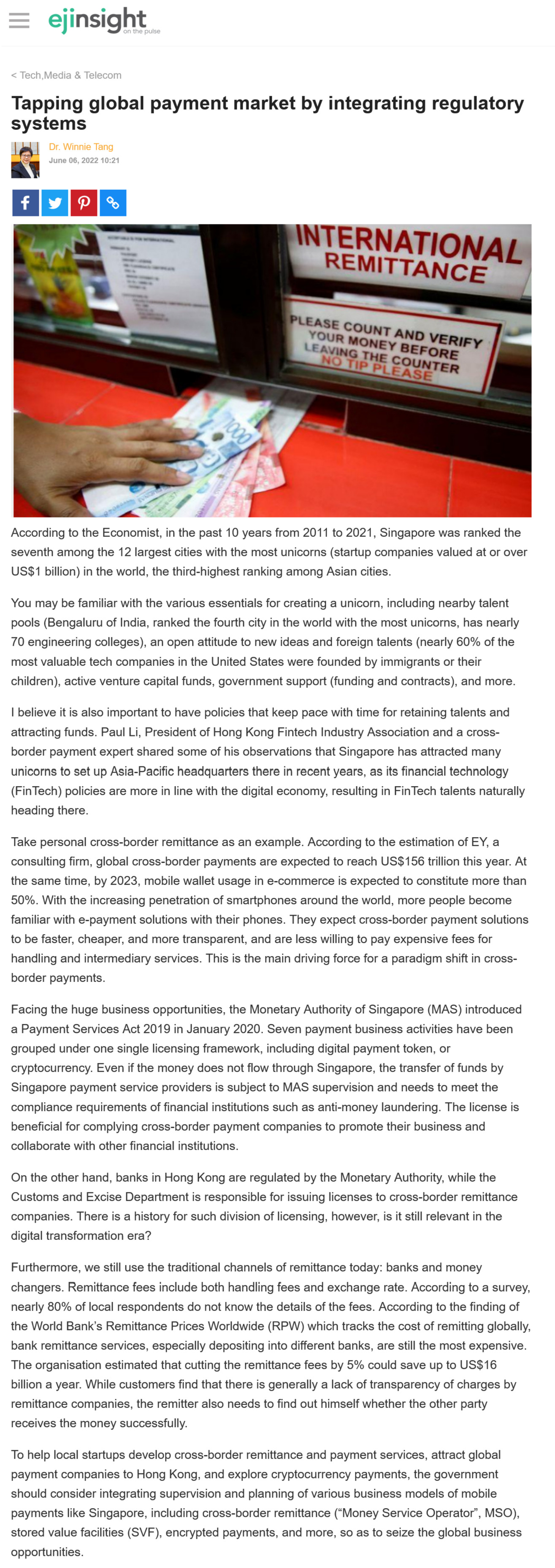

Take personal cross-border remittance as an example. According to the estimation of EY, a consulting firm, global cross-border payments are expected to reach US$156 trillion this year. At the same time, by 2023, mobile wallet usage in e-commerce is expected to constitute more than 50%. With the increasing penetration of smartphones around the world, more people become familiar with e-payment solutions with their phones. They expect cross-border payment solutions to be faster, cheaper, and more transparent, and are less willing to pay expensive fees for handling and intermediary services. This is the main driving force for a paradigm shift in cross-border payments.

Facing the huge business opportunities, the Monetary Authority of Singapore (MAS) introduced a Payment Services Act 2019 in January 2020. Seven payment business activities have been grouped under one single licensing framework, including digital payment token, or cryptocurrency. Even if the money does not flow through Singapore, the transfer of funds by Singapore payment service providers is subject to MAS supervision and needs to meet the compliance requirements of financial institutions such as anti-money laundering. The license is beneficial for complying cross-border payment companies to promote their business and collaborate with other financial institutions.

On the other hand, banks in Hong Kong are regulated by the Monetary Authority, while the Customs and Excise Department is responsible for issuing licenses to cross-border remittance companies. There is a history for such division of licensing, however, is it still relevant in the digital transformation era?

Furthermore, we still use the traditional channels of remittance today: banks and money changers. Remittance fees include both handling fees and exchange rate. According to a survey, nearly 80% of local respondents do not know the details of the fees. According to the finding of the World Bank's Remittance Prices Worldwide (RPW) which tracks the cost of remitting globally, bank remittance services, especially depositing into different banks, are still the most expensive. The organisation estimated that cutting the remittance fees by 5% could save up to US$16 billion a year. While customers find that there is generally a lack of transparency of charges by remittance companies, the remitter also needs to find out himself whether the other party receives the money successfully.

To help local startups develop cross-border remittance and payment services, attract global payment companies to Hong Kong, and explore cryptocurrency payments, the government should consider integrating supervision and planning of various business models of mobile payments like Singapore, including cross-border remittance ("Money Service Operator", MSO), stored value facilities (SVF), encrypted payments, and more, so as to seize the global business opportunities.

Dr. Winnie Tang

Adjunct Professor, Department of Computer Science, Faculty of Engineering; Department of Geography, Faculty of Social Sciences; and Faculty of Architecture, The University of Hong Kong